Many people put the idea of early retirement to one side because it seems so unobtainable. How could you ever save enough to retire early when you’re not earning £100k a year? I used to have that mindset, sure I’ll put money into my pension but it will be a drop in the ocean. There are no big areas of spend for me to cut, so why bother looking? Making small savings just won’t have the impact I need.

But actually even saving a small amount regularly over a long period of time has an amazing impact on funding our pensions.

Regular saving & time = lots of money

Firstly that small regular spend we have adds up to a much bigger number when you look at it over a year. If you spend £3 every day on a coffee that doesn’t sound much does it? Well over a year, if you buy that coffee every day, you would have spent £1,095. That is a big chunk of money! If you earn the average salary in the UK of about £27k than that is 4% of your salary!

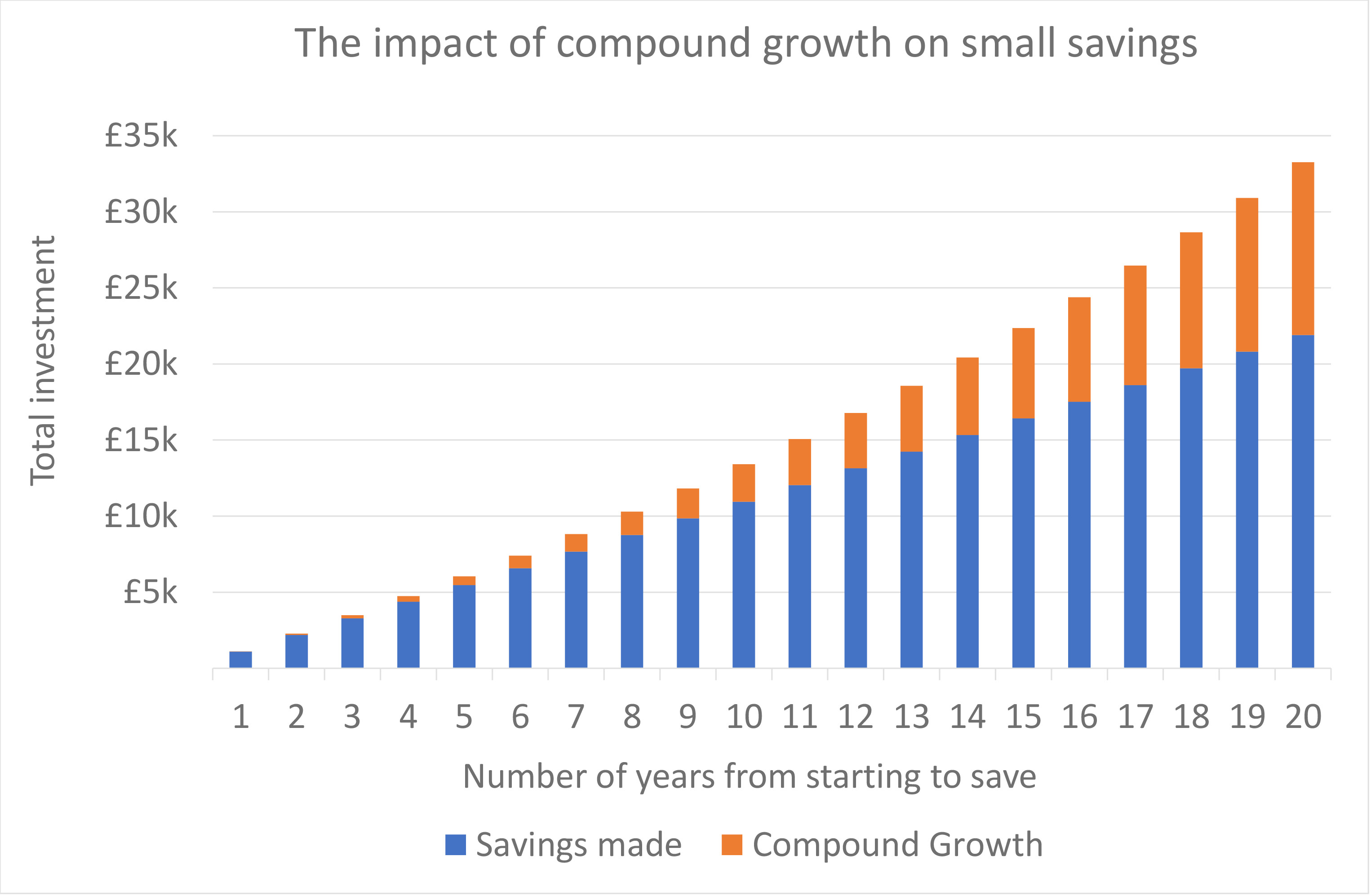

But that’s not the whole story because we’re likely to be retiring more than a year away. That £1,095 doesn’t just grow each year through your savings, but from the compound growth that your investments should return. The chart below shows how saving £3 a day grows could grow to be worth £13,410 in 10 years, or an amazing £33,259 in 20 years!

Make a choice – spend or save

Many people take no care of their money till they come nearly to the end of it, and others do just the same with their time.

Johann Wolfgang von Goethe

Of course you might turn around and say “David! That coffee is one of the highlights of my day. It’s the one treat I give myself.”. That’s fine. I’m not saying we have to cut every single expense from our lives, live like hermits wearing clothes that are 20 years old and forage in bins for food.

But I am saying that for everything we spend we should weigh up what we get out of it. What pleasure does it bring? What does it add to our life? And then compare that to the potential additions to our pension pot we could make by cutting the spend.

After my first check on we were progressing towards retiring in ten years I found out we were slightly off the pace for our “perfect” retirement. So I did another check on my outgoings to see where I could cut more. One thing stood out, my daily work lunch at Itsu. My chicken noodle soup is super tasty and healthy, but it also costs £4. That’s £4 every day, and £20 a week. What if made my own lunch and saved £3 every day?

I worked out that in ten years that would add up to £8,413. You really see the impact if you increase the timescale further. If I worked up to my statutory retirement age (26 years to go) then I would save £31,051. Assuming I then drew down from my pension at 3.5% a year that would be the equivalent of an extra annual income of £1,087. And don’t forget drawing down at 3.5% means that the £31,051 should hold its value.

For me, the Itsu had to go. It’s not a game changer, but it will plug some of the gap that I’ve currently got if I’m going to reach my goal of having the perfect retirement in just ten years.

So what areas of spend do you think you could cut back on to help kick start your retirement fund?

See you much your investments could grow with small savings!

Being able to visualise how much you can save by reducing your spend is really helpful. It makes it much easier to make the initial decision to stop spending on something. It also makes it much easier to to stick to it and not buckle at some point in the future.

To help you I’ve created a ‘small savings big impact’ spreadsheet that will show you the impact of making small adjustments to your life, and how much you could save by the time you retire. You can read more about it in the resources section and get free access to it if you sign up to the weekly newsletter.