The first state pension in the UK was the Old Age Pension. The law was passed in August 1908 and the first pensions paid on 1 January 1909 to around 500,000 people aged 70 or more. At the time only one in four people reached the age of 70 and life expectancy at that age was about 9 years.

One thing you may not know is that you can boost your UK state pension by deferring when you take it. The obvious question is, does it make financial sense to defer your UK state pension? And even if not, are there any circumstances you might want to defer it?

If you are thinking of deferring your state pension you should check out the gov.uk website to make sure everything is still as explained in this post. You don’t actually have to do anything to defer your pension as you will be contacted a few weeks before you are due to receive your first payment. At this point you need to confirm you want to start to take your pension.

If you are rushed for time, then you can jump right to the conclusion. Otherwise we will work though the options and outcomes together.

Does it make financial sense to defer your UK state pension?

Before we dive into the number crunching let’s see what the actual benefit is of deferring your pension. Basically for each 9 weeks you defer your pension you will get a 1% increase on the amount of pension you would have otherwise received. This is about 5.8% if you defer for one year. A person receiving a full state pension of £8,546.20 (2017/18) would therefore receive an extra £493 for deferring one year, a total of £9,039.20.

In order to compare the different options I’ve assumed that in each scenario the money received from the state pension will be invested. I’ve modeled the impact of deferring by one year and two years. This is then compared to the position you would be in had you not deferred the pension. So all of the charts I show display the difference between deferring and not deferring the pension. A retirement age of 67 and a full pension is assumed. You may have a different retirement age to this, or not recieve the full state pension.

The first chart to the right shows what happens assuming a 0% growth on investments. Let’s look at the blue bar, which represents deferring your pension 1 year, and see what it shows us:

- In year 1 if you were to defer your pension you would forgo £8,546 (2017/18) in your first year, and so we have that as our starting deficit.

- The point when the blue line crosses 0 on the graph is when you are no better or worse from deferring your pension. In other words you need to make sure you live this long for it to be worth doing!

- It will take 220 months (18.3 years), so you will have to live longer than 85 to be better off deferring the UK state pension one year.

- If we look at the orange line we can see that you would need to live longer than 86 to be better off deferring the UK state pension two years.

An average male aged 67 now, is currently predicted to live to roughly 84, and the average woman 86. So (using a 0% return) on average there is no financial benefit in a man deferring their state pension, whereas the average woman would be £424 better off. Unless you have particularly good genes you aren’t likely to see much of a benefit in other words!

What about the impact of compound growth on the calculation?

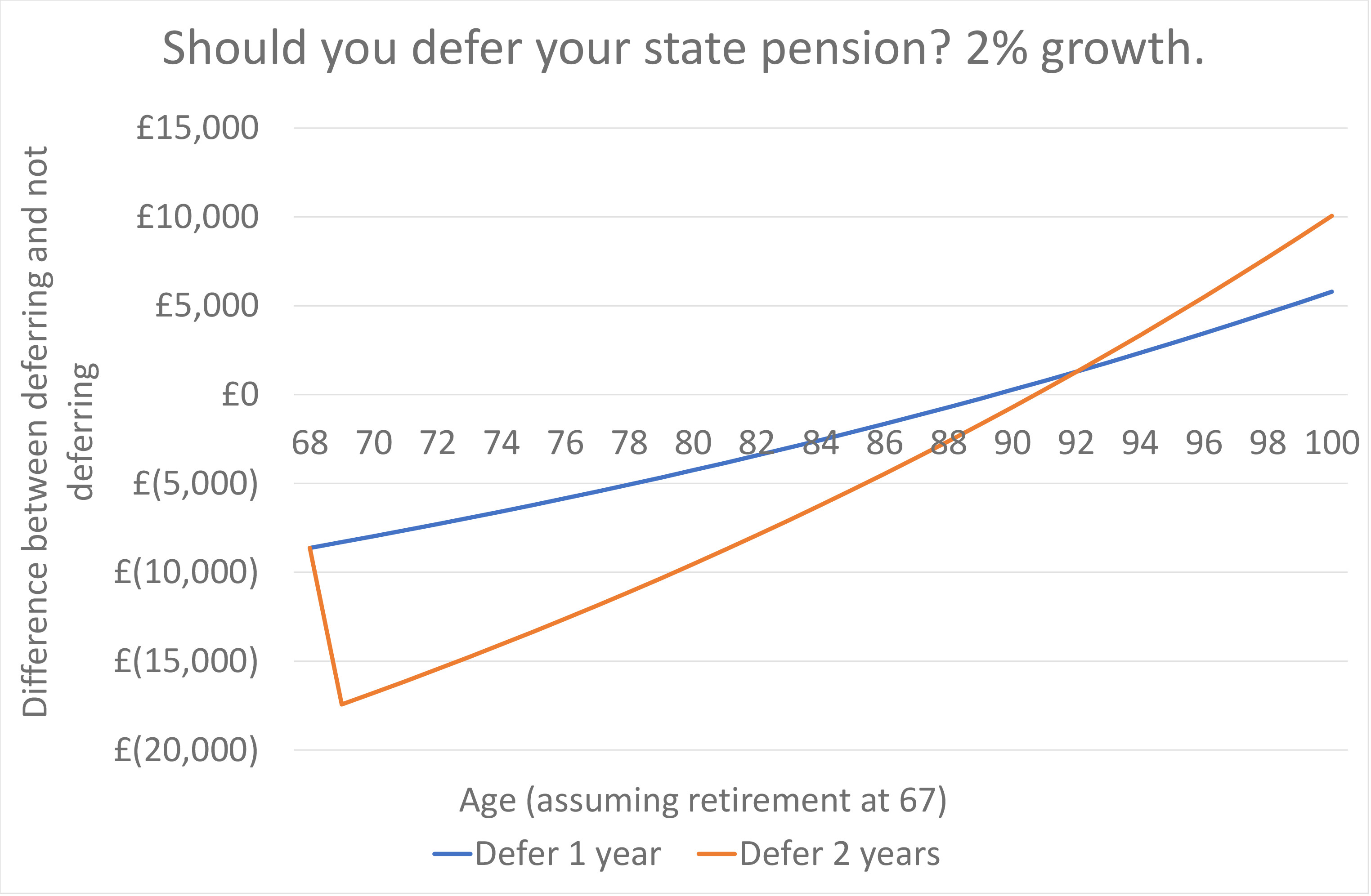

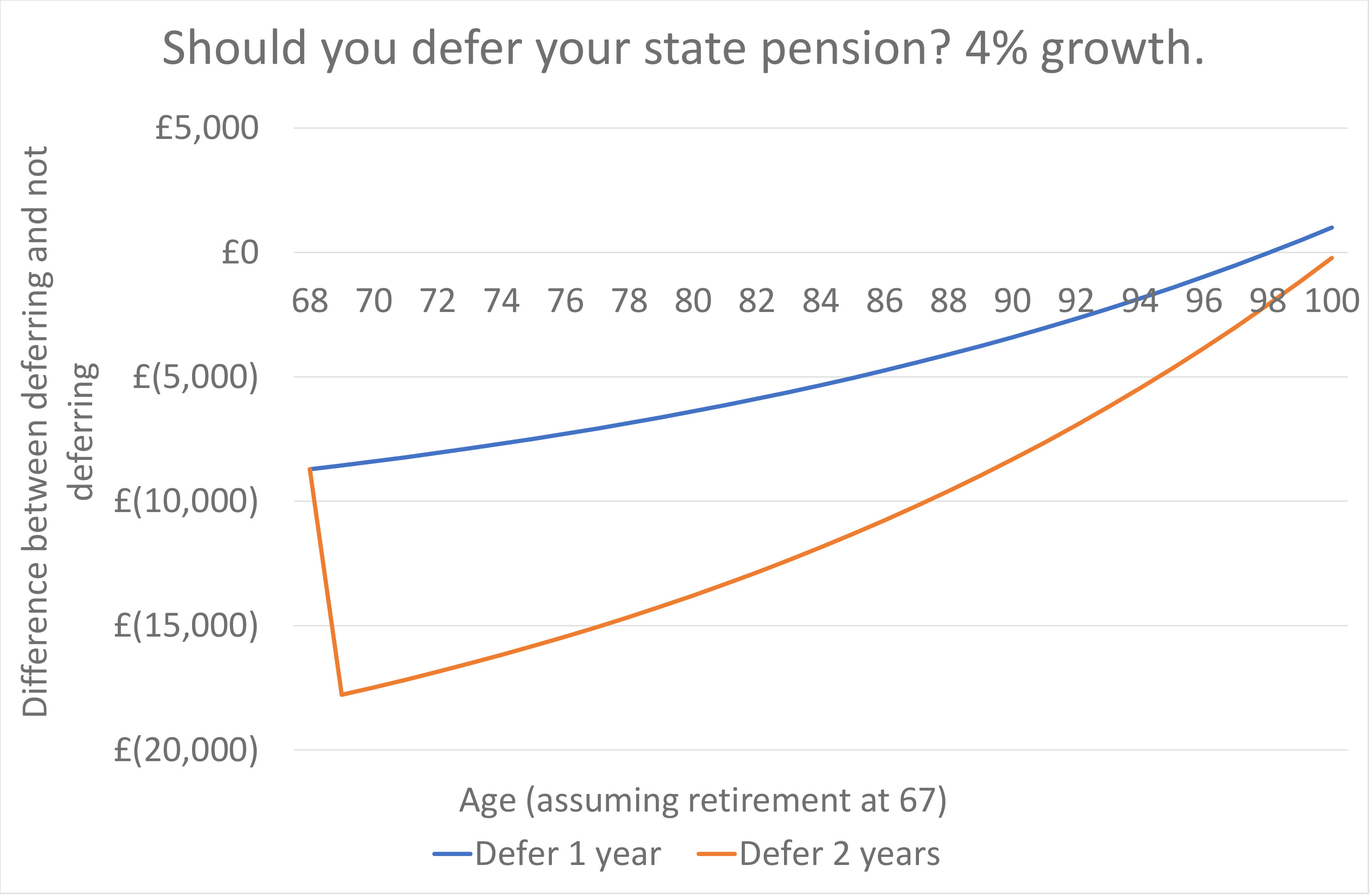

However the above calculations need to be refined a little to take into account that we would expect any money invested to generate a return on investment. The two graphs to the right show the results if a 2% annual growth and 4% annual were achieved. As you can see in both scenarios including growth of investments increases the age you would need to live in order to benefit financially from deferring your pension. This makes sense as with 0% growth until you do reach the break-even point you will always have more saved by taking your retirement. As soon as we start adding in growth to our investments it quickly improves the decision to draw the pension as soon as you are eligible.

Here are the new ages where the decision to defer breaks even:

- With a 2% growth in investments

- Deferring 1 year you would need to live to over 89 years old

- Deferring 2 years you would need to live to over 90 years old

- With a 4% growth in investments

- Deferring 1 year you would need to live to over 98 years old

- Deferring 2 years you would need to live to over 100 years old

Okay, now it really doesn’t look very appealing at all! Most people would expect a growth in their investments of at least 4%. If you apply that logic here then you would have to live to 100! It is therefore fair to say that this bit of analysis is a massive nail in the coffin* of deciding to defer your UK state pension. If you decide to defer your pension then from a purely financial perspective – it is not a good choice. Don’t do it.

* this is probably a slightly inappropriate phrase given the topic!

But I don’t need the money yet, shouldn’t I defer it until I need it so I get more?

In a word, no. What you should do in this situation is take the pension and then invest the payments as you receive them. This way you should end up with a better return than if you were to defer the payment.

Why might you want to defer you pension?

So from a purely financial outlook, we have seen that it doesn’t stack up. However there are some circumstances that might make you still decide to take this option.

1. It can reduce risk by increasing your fixed income

Not every decision we make in life is 100% about whether it gives us a better financial outcome. Sometimes we will take a worse overall outcome if it provides certainty and a guaranteed income. As a couple the state pension will provide an income of £17,092 every year – no risk. If a couple were to defer their pension for 2 years then they could boost that up to £19,064, or £20,052 if they deferred for 3 years.

If that extra £2k-£3k a year guarantee helps you sleep better at night, then that might well be a reason to decide to defer.

2. It could be better than an annuity

The chances are that you’ll find that deferring your pension is a better approach than taking out an annuity. The chart to the right adds a line showing the decision to take out an annuity providing £1,000 income per year. I’ve assumed you can get the annuity for £20,000, which is equivalent to a 5% rate. You’ might struggle to get a joint annuity for this rate, If you couldn’t then the green line would be worse/lower. This annuity is effectively the same extra income per year as it is to defer your state pension by 2 years as they both provide c£1k per year. As you can see the green annuity line is always the lowest on the chart.

The maths here is pretty simple when we break it down.

- To get the £986 extra income boost to your retirement, you would give up two years worth of pension which would cost you £17,092.

- To get the annuity of £1,000 per year would cost you £20,000. You would also benefit from two extra years income at the start, which in effect bring the cost down to £18,000.

- But of course if you didn’t take out the annuity you’d still have £20,000 sitting in your investments. With a 4% return you’d be loosing out on £800 a year, almost wiping out the benefit of the to year extra income at the start.

For the annuity to give the same return as deferring your pension 2 years you would need an annuity rate of 5.42%. Importantly though this doesn’t take into account inflation. Firstly any annuity would need to be linked to inflation as the state pension will increase every year by at least inflation due to the triple lock rules. If the government doesn’t revoke the triple lock rules then you might need annuity rate of up to 6.3% to keep track. Good luck finding that annuity!

Obviously there is a limit to how much you can earn per year deferring your pension, about £1,000 a year if you are a couple. The good thing about this approach is that as soon as you reach your retirement age you can get quotes on annuities. Therefore you will know exactly what the best option is depending on the quotes you get. As you can read elsewhere on this website, it is almost always going to be better not to take out an annuity.

3. It will make 100 a super special year!

Look, if you live to a hundred I think that deserves a celebration! Sure you will have your family around you and have a party. And if you live in the UK you’ll get a letter from queen or king (see image to the right), unless cost cutting measures have stopped this by then. But what better way to celebrate than to know that it did make sense to defer your pension for 2 years! Ha, you knew you were right not to listen to that bloke on some website you stumbled upon!

Conclusion – should you defer your state pension?

No. You will almost certainly be better off financially by taking the state pension as soon as you can. Even if you don’t need the money, take the pension immediately and then invest whatever you receive.

The only circumstance it makes sense to defer your UK state pension is if you are really looking to get a higher guaranteed income. Each year a person defers their pension it will increase by £496. You will probably find this is also a better option than taking an annuity. But note the first comment, you will be trading your overall financial health for certainty.