It’s all well and good knowing how big a pension pot you need to retire on. But this naturally leads onto the next question. How on earth can we get there! A key part of reaching financial independence is how to save more money. This website will help give you some help in achieving that.

Because ultimately, being able to save more, will be one of the biggest factors on when we can retire. And how well we can retire. If I want to retire I know I need to be in control and taking responsibility for getting there. If I happen to win the lottery* before then then sure I’ll change my plans, but until that happens its down to me.

I need to be proactive in saving as much money as I can.

*Playing the lottery is not a recommended route for retiring early, unless you can guarantee a win.

So, how do you save more money?

Not surprisingly it boils down to two things…

- earn more money

- spend less money

Conventional wisdom follows this chart. Savings = Income – Spend.

This is logical. We start by earning money in our job. Then we spend money on lot of stuff. And if we’re lucky we end up with some money left over that we can save.

We can only save what we earn or receive. And what we earn or receive is reduced by how much of it we spend. We need to squeeze as much of a gap between what we earn and what we spend so that we can invest and save the rest.

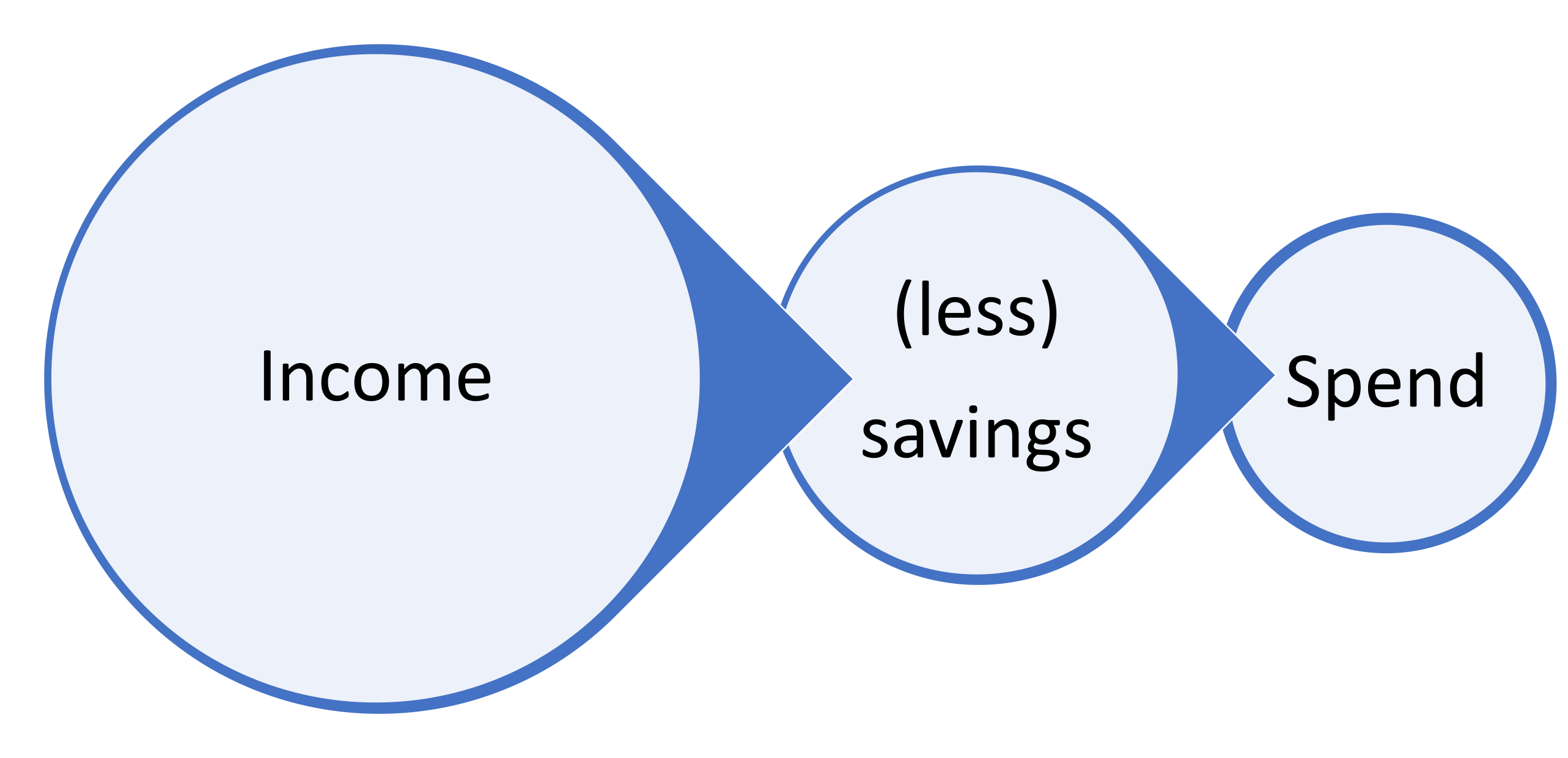

The super saver’s wisdom follows the next chart. Income – Savings = What I can spend

The underlying algebra is the same, but the focus is different. Saving takes priority over spending. Don’t wait until the end of the month and see what you have left that you can save.

Set a savings target and adjust your spend to fit it.

Many people aiming to retire early advocate a savings rate of 50% of income. That can seem utterly impossible at first. And maybe in the short term it is. But by making continual improvements to both your income and you spend you can certainly get closer. And who knows, maybe you can even exceed 50%.

So how can I earn more money? What side income ideas work?

Earning more money is undoubtedly a powerful way to boost the amount you can save. Many people find their spending naturally increases as they earn more,

- They go on better holidays,

- Their houses get upgraded,

- Eating out happens more and more often.

But it doesn’t have to be that way. Re-investing any additional income you can earn is a sure fire way to speed up your early retirement.

Earn more in you current job

If you’re working 45 hours a week in a job then that is going to be a large chunk of your productive time. Focusing on booting that income should be a starting point.

This is can difficult area for many of us to broach. How do you ask for a pay rise? What techniques can make you more valued in the workplace?

This is not an area I’ve started to look into yet in my path for early retirement. But there are some useful guides available. This post at ESI Money is particularly useful in having the right mindset at your place of work.,

Move jobs

One thing does often hold true is that moving job can often help..

It is normally much easier to get a pay rise by moving to another company rather than staying put. This could be the case either if you are looking for a promotion or even staying at the same level. Any advertised job will be more likely to offer the market rate.

Earn more by finding what side income ideas work for you.

Earning additional money from side income ideas is also a great way to provide additional funds to boost your savings. Side income is basically income from something you do that isn’t your main job. It could be anything. Literally anything. From dog walking, to running a website, to selling stuff you make.

You may find that you’ve hit a ceiling in your current career and can’t earn more. In which case this is the easiest way to earn more money.

Perhaps more compelling is that you can start to build an income stream that you will continue when you gain financial independence. In the short term you will benefit from extra income that you can save. But furthermore you get the huge benefit of an extra income stream in your early years of retirement.

Preferably you will also be making income doing something you enjoy. Something you want to continue when you retire.

What money saving tips do have to help me spend less?

Spending less of your hard earned money will certainly help you to retire earlier. It may seem impossible right now to save any more, or even to save anything. But often there are things that can be done. Some of these money saving tips will be easy for you to implement. Others you may just not be willing, or able, to achieve.

There will be limiting factors for each of us either through circumstance or lifestyle. For me one lifestyle perspective I’m not willing to forgo is holidays for ten years to retire a bit early. That’s not fair on my family. But how much do I need to spend on my holidays? Which holidays bring most most joy to our family?

We will all have different “limiting factors”. And that’s fine. But we will also all be able to make changes to our lifestyle to reduce our spend. Of all the money saving tips I could give it would be don’t waste money on stuff that doesn’t bring you joy. That may seem obvious, and yet if we don’t control our expenditure – that is exactly what we will do.

So here, very summarised, are some of the key money saving tips:

Know how much you spend

Actually knowing how much you spend is a vital first step. Yes, you can cut your spend without doing this. But most likely you will underestimate how much you are making on certain areas. You will have forgotten about that monthly subscription to a service you don’t use any more. And you won’t realise just how much you spend on certain activities over a month.

Some people track their spending every month in detail. I don’t have the patience for that. But at the very least I suggest you try to do a ‘1 month audit’. Jot down what you spend on different things over a month

Cut out or reduce spend that doesn’t bring you joy

Okay I know, that sounds a bit wishy washy. But I would always start by getting some quick wins that will have zero impact on your life. There are some things we spend on that bring us joy (think going out with friends). There are others that don’t (think electricity bills, broadband).

Many companies providing what are effectively commodities have an inherent practice of overcharging loyal customers. You should check all of your utility contracts, mortgage provider, insurances, phone and broadband contract, and other similar services. What difference does it make to me if I pay my mortgage to Bank A rather than Bank B? None. But if I can pay 1% interest rather than 3% on a $300k loan that’s going to be a $2,000 saving every year.

A long as you are getting the same level of service, then you should review what you can save by switching providers.

But reducing spend that doesn’t bring joy goes further than that. You should run the rule over every area of spend and ask just how much it really adds to your life.

A report four years ago showed that the average person at work spend almost £6 a day on their lunch and coffees at work. Okay, we need to eat. I’m not suggesting a daily fast. But when look at the quality of food I’ve eaten over the years at my lunchtimes, it is generally quite depressing. I love my food. I don’t love dry sandwiches and bland salads. And yet on average people pay £1,500 a year on their lunch. That’s £1,500 a year something that may just be done out of convenience. Would you be willing to make your lunch yourself? Have a better lunch, and save over £1,000?

Most things in our live that bring us joy tend to be things that cost less. Yet as a society we’ve got used to spending. To accumulating stuff.

Reduce your debts

You should focus on reducing your debts as soon as possible. This is particularly true for debts that have a high interest rate on the such as credit cards or store cards. But less so for debts such as mortgages where you may find you get a higher return investing than you are paying on your debt.

If you are spending $500 every month on servicing a loan for that huge fridge you just had to have… then that is $500 you can’t invest.

Debts also add more risk to your current lifestyle. If you were to lose your job you could stop eating out. You could cancel your Netflix subscription. But you can’t stop paying back your debts.

Don’t neglect the power of reducing seemingly small areas of spend

It is very easy to dismiss cutting down on certain areas of spend because you think it just won’t have an impact. But actually regular small spend can have a surprisingly big impact over a long period of time..

Let’s imagine you spend £3 a day on a coffee. Big deal. £3 doesn’t make a pension pot.

But over a year, if you buy that coffee every day, you would have spent £1,095. For the average person in the UK that is 4% of their salary. On coffee. On coffee from a place that makes huge profits and probably pay less tax than you.

And what happens if you invest that £3 a day?. That £1,095, through compound growth, it grows and grows and grows. In ten years you would have £13,410 saved. In twenty years it grows to £33,259!

So just how much do enjoy your shop bought coffee?

Ask challenging questions on your larger areas of spend

You should also make some challenging decisions about your largest areas of spend. You could find a few years of changing your lifestyle will have a big impact on how much you can save. Could you move to a cheaper area, or a smaller home? Do you need a car or can you get to the places you need on public transport?

Some of these could be more difficult decisions to make, and often the answer may be no. I do need that car, I can’t lower my housing costs.

But if you do have flexibility then weigh up the cost.

- Would you rather retire earlier?

- Or would you rather make some lifestyle changes now?

Asking those two questions about most areas of spend will often lead you to the correct answer, for you, on whether you should cut/reduce spend. Or continue and enjoy the benefits it brings.

Hopefully these money saving tips will help you save more. And as you browse through the website you should be able to glean more.

Surely you’ve done the hard work now and can sit back and enjoy the spoils of your effort?

This is probably is one of the harder steps for most of us. But if you want to reach financial independence then you can’t be the only one working hard. You need to make sure your money works hard for you as well. In the next step we’ll take a look at how you can make sure every penny you squirrel away grows even if you were to stop contributing to your savings.