The number of investment options can be very bewildering even to the financially literate. If you have put off investing due to fear or confusion then this post is for you.

I remember starting my first job and receiving the paperwork to join the work pension. I was starting a career in accounting but this just went over my head. I had to pick from a list of about 200 funds where I wanted to invest my pension. I didn’t have a clue so procrastinated for a couple of months before finally just guessing what to chose.

Things have certainly improved from an accessibility point of view now, with most schemes giving you a few clear options unless you want to spend the time creating a bespoke portfolio for yourself.

The tagline for this post is – keep it simple. If you want more depth then you can find other articles on this website. But if you just want to start investing and are confused, this is your starting point.

Don’t let fear stop you from investing. Keep it simple.

This fear can also stop us from knowing what to do with any cash that we have started saving. Where do you start? Cash ISAs (Individual Savings Accounts) are popular because they very low risk, and it is an easy choice to understand. Unfortunately the low risk means that with interest rates well below inflation at the moment Cash ISAs are not an investment, they just keep your cash safe as it slowly dwindles in real value. Do you have that uncertainty and fear? Well, the main takeaway from this post is to KEEP IT SIMPLE.

If you can’t be bothered to read anymore and just want to do it – do this:

- Decide to invest in a stocks and shares ISA

- Set up an account with Hargreaves Lansdown or Vanguard.

- Pick an exchange-traded fund (ETF) with them (e.g. Vanguards The LifeStrategy® Equity Funds)

- Start investing your hard earned money!

If you want a little bit more background then read on…

Get the basics right – be tax efficient and use an ISA

An ISA (Individual Savings Account) is a tax-free way to save or invest. If you’re starting to think about saving or investing, ISAs could be a good place to begin.

There are some fundamentals that you do need to get right first, the main one being to make sure your savings are tax efficient. We will look at this in more detail in another post, but you should make sure you’re first of all investing in a company pension if you can. This is especially true if you’re a higher rate tax payer. For this post I will assume you’ve done all that though and now have some cash every month you want to start investing. You might not have maxed out your pension, particularly if you know you will want to access some of your investments before your earliest retirement age. The earliest I can retire is 57 (and 1 month), I’m planning to retire at 51, so that means I’ve got about six years I need to cover.

Your first step should always be to either invest more in your pensions, or as much as you can in stocks and shares ISAs. You can put up to £20k per year (2017/18) into ISAs. That is £20k per person so if you are a couple you can invest up to £40k a year in a tax efficient investment. Not too many of us will be at the level of breaching that amount, but until you do put everything you save into ISAs. NB you can only have one ISA each tax year so once you have started, you need to stick with that. If you’ve already started a cash ISA this year don’t worry – you can always transfer it next year.

With an ISA you get the benefit of it being tax efficient when you come to draw down some of the savings in the future. In other words you won’t be taxed on any of the income when you take it from your ISA. This is different from investing in a pension which is a taxable income when you draw it, but with a pension you get the tax relief when you make the initial deposit.

So that was simple – save your money in stocks and shares ISA

Who should you put your investment with? Keep it simple.

Again there are many choices about which institution you could use. I will cut to the chase and suggest you start with either Hargreaves Lansdown or Vanguard. These were both highly recommended across several independent reviews that I read. We currently have a private pension with Hargreaves Lansdown and Share ISAs with both Hargreaves Lansdown and Vanguard (one in my name, one in my wife’s). The main reasons for choosing these are,

Again there are many choices about which institution you could use. I will cut to the chase and suggest you start with either Hargreaves Lansdown or Vanguard. These were both highly recommended across several independent reviews that I read. We currently have a private pension with Hargreaves Lansdown and Share ISAs with both Hargreaves Lansdown and Vanguard (one in my name, one in my wife’s). The main reasons for choosing these are,

- Both have exchange-traded funds (ETF) with low charges. This is the type of fund we want to invest in (see the next section).

- They don’t have high fees for managing the index funds, or for changing your investment.

- The websites are both pretty simple to use and user friendly

- Both are well respected in the industry

Feel free to investigate a wider market, but if you’re looking for a quick option then go with one of these two institutions to get the ball rolling.

What type of stocks and shares ISA should I get? Keep it simple.

Just like my first pension though there are countless different options available with stocks and share ISAa. You can invest in:

- Unit trusts

- Investment Funds

- Exchange-traded funds

- Individual stocks and share

- Corporate and government bond

- Open Ended Investment Companies (OEICs)

Oh no – it’s not so simple now, especially as within each of these categories there are then loads of other different choices. Fear not though – there is an easy answer!

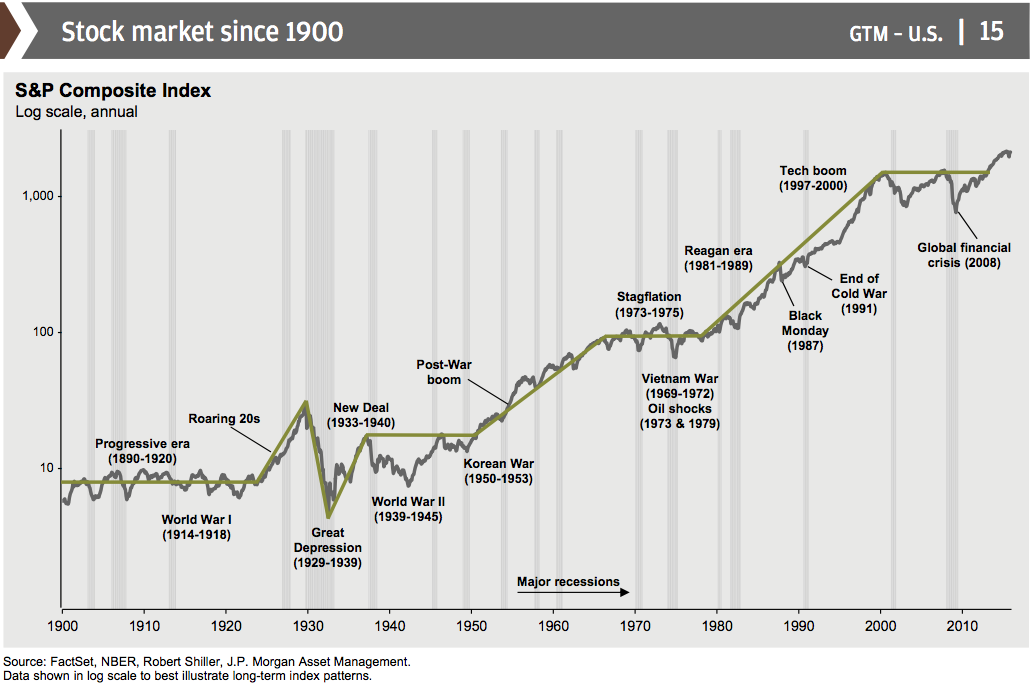

Only a fool would not want to maximise their returns on any investment. The trouble is it’s difficult to achieve that. Many professional investors struggle to beat the average returns of the stock market. Thankfully we don’t need to be trying to get double digit returns returns to benefit from compound growth. The chart below shows the growth of the US stock market over the since 1990…

An ETF (exchange-traded fund), is a security that tracks an index, commodity, bonds, or a basket of assets like an index fund. Fees are low for ETFs as they are trying to track the market rather than beat it.

It has certainly not always been plain sailing, but if you hang in there you will get a return. Of course we could have another great depression which would put paid to my early retirement! So unless you are really going to spend your life researching for the next best thing, and then get that right, you need to find something that will track the stock market. With the timescales involved planning for retirement you should have plenty of time to ride out the bumps. It’s often recommended you expect to keep funds invested for a least 5 years to ride-out this risk.

Thankfully there are options that fit this bill. They are called Exchange-Traded Funds (I’m sure you guessed that by now!), and they are effectively a bundle of shares representative of that markets they are invested in. This removes the risk of investing in individual shares, and also means the baskets of shares can include emerging markets, UK, US, and Europe all in one investment. Exchjange-Traded Funds also tend to have low fees which make them even more attractive.

How much risk do I take? Keep it simple.

Life is inherently risky. There is only one big risk you should avoid at all costs, and that is the risk of doing nothing.

Denis Waitley

Once again in the interest of simplicity I will keep this section brief. We all have different degrees of risk we’re willing to take. Partly due to our life circumstances, but also inherently who we are as people. You need to pick an investment that you are comfortable with. If you’re aiming for early retirement you don’t want to spend every day fretting about your investments.

Therefore whilst sticking to to the Exchange-Traded Funds it is common to pick funds that have a mix of both bonds and shares. Bonds have a lower potential return than shares, but they are less risky and also tend to do better when shares are in the doldrums. Both Vanguard and Hargreaves Lansdown package their trackers to allow you to pick the level of risk. You might want to consider something like this:

- Low risk: 40% Shares – 60% bonds

- Lower risk: 60% Shares – 40% bonds

- Higher risk: 80% Shares – 20% bonds

- Highest risk: 100% Shares – 0% bonds

You may not have a clue what your risk appetite is! That’s fine. But if you’re going to spend six months existentially trying to work out just how risky you are, then you need to make a choice. I can’t advise you, but if you are unsure then I expect you might feel more comfortable starting with a less risky portfolio. I’ll investigate this more in future articles, but the whole point of this article is to keep it simple. To get you investing.

Assuming you are going to plump for Hargreaves Lansdown or Vanguard then they both have suitable choices. Vanguard have The LifeStrategy® Equity Funds that are easy to select, whilst Hargreaves Lansdown provides a bit more flexibility.

What if I change my mind?

So after a few months you’ve done more research and feel a bit more comfortable making decisions. And you realise that the product you picked was either too risky for you, or not giving enough potential for high returns. What will you do?!?

Thankfully you can change your mind really easily. Just make sure you choose an institution that will allow you to transfer money for a low (or no) cost and you are fine. If you decide take a different approach once you are more confident in investing then you are free to do so. You can transfer into another ISA without it counting towards your annual limit (just make sure you do it properly). You are not fixing yourself into any long-term commitments here.

I moved my first portfolio to different products within my Vanguard account a month after doing more research. At no cost. Should I have taken my time before making that first leap? No! By making that first step I was suddenly invested (literally) in the outcome of my funds. And that was what made me do more and more research. I also happened to make over £200 in a month, although that was obviously largely due to lucky timing. But what is certainly true is that the longer you leave investing, the longer you are forgoing potential future growth.

How simple is that!

There is so much more that could be written on this area, and I will be looking further into all of them over the coming months.

There is so much more that could be written on this area, and I will be looking further into all of them over the coming months.

But the main thing to take home from this article is to try to keep it simple wherever possible. Unless you have happen to be a financial guru your best bet is to find something that works without lots of work. Then you can relax and enjoy your drink of choice.

And that simple plan is,

- Decide to invest in a stocks and shares ISA

- Set up an account with Hargreaves Lansdown or Vanguard.

- Pick an Index Fund (ETF) with them

- Start investing your hard earned money!

While I may be reading this from across the pond, the message of simplicity still rings true. I too had a moment of baffled indecision and dartboard investment, but through the power of simplicity I was able to feel confident in my first step.